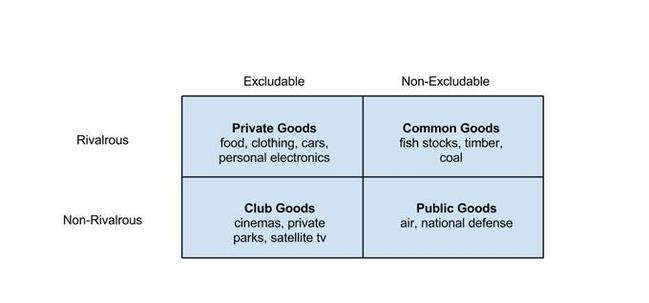

Hello! In my last blog post we talked about supply, demand, elasticity and the importance of markets economy. However, some markets do end up being imperfect and inefficient. Today, let's tackle the topic of Market Failure. In economics, Market failure, as the name suggests, happens when the market fails because it is inefficient - that is, not operating at its maximum and optimal capabilities. There are many possible reasons why a market would fail, one of which is the existence of externalities. The global issue I’d like to use as an example is the topic of overpopulation and how market failure arises from that and the free rider problem. To understand the free rider problem, we have to know about externalities first. Externalities are the indirect effects of a particular activity (either production or consumption of a good or service) that influence a third party. This third party is not paid by those who engage in the activity nor is paying them. Externalities can thus be classified as either positive or negative. An externality is positive when the third party benefits from this action. An example of a positive externality is education. Education increases the amount of experienced and intellectual citizens which may lead to positive changes in society like a low unemployment rate. On the other hand, an externality is negative when the third party suffers/harmed as an indirect effect of an action. The best examples for a negative externality are pollution and global warming - caused by the burning of fossil fuels in the factory production of various goods. This activity then results indirectly in carbon emission in the atmosphere, which then globally harms humanity. The important thing to note about externalities is despite them being indirect/unintentional, externalities are still reflected in the price of an object. If a product has a negative externality, it is very likely that the product’s price would increase as a result while products/services with positive externalities tend to be encouraged via subsidies and such. To better understand externalities, let’s talk about the kinds of goods. These are public goods, private goods, club goods and common goods. There are two questions to ask when classifying these, “Is the good a rival in consumption?” and “Is the good excludable”. A good is excludable if and only if the people who have actually paid for the good are the ones who use it. A good is a rival in consumption if the consumption of that particular good is contested - meaning the more one good is used, the less other consumers can use it as well. Let’s talk about each one in depth:

These kinds of goods relates to externalities because in essence, these kinds of goods are classified also based on their externality on people. However, let’s focus on public goods as it directly relates to the free rider problem.

The free rider problem arises when people receive positive externalities from a particular good but don’t actually pay or contribute to the creation/production of these free goods, in other words, these “free riders” get more than what they deserve. This is a problem because these public goods will run out if the producer does not get compensated for their work. That and the people involved don’t actually contribute to the efficiency, leading it to become inefficient. Thus market failure occurs. A great example of this is when a government actually does its’ job and use taxes to provide new infrastructure BUT people stop paying taxes, meaning that these people don’t actually contribute anything to these new infrastructures yet use them anyway. The government is then left with no funds to continue creating more public goods. Personally, this means that people should stop complaining about these public goods or blaming the government, if they don’t actually pay taxes and try to help. Now let’s link it to the global problem of overpopulation. As mankind progresses through history, more people will undoubtedly be born. However in recent times, humans have been multiplying at a higher exponential rate, thus leading to overpopulation. Now the problem with overpopulation is that it leads to a concept called “tragedy of the commons” wherein people independently without a care for other people; in other words, they deplete these public goods selfishly. Overpopulation then leads to the free rider problem because more and more people actually take more than what they deserve and cause more damage, in light of their self-fueled desires. More people will then take land (sometimes even destroy the land) for themselves, leaving less or even none for the rest of us. Hopefully, this economics blog helped you be more aware of the externalities each of our actions bring and brought to light the problem of overpopulation. References & Sources: https://www.boundless.com/economics/textbooks/boundless-economics-textbook/market-failure-public-goods-and-common-resources-8/public-goods-61/defining-a-good-229-12320/

0 Comments

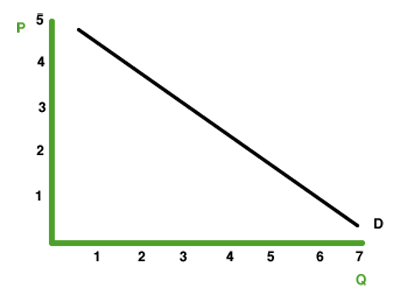

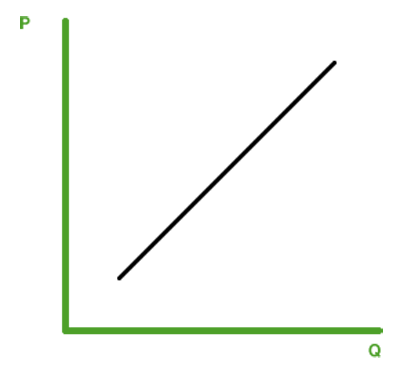

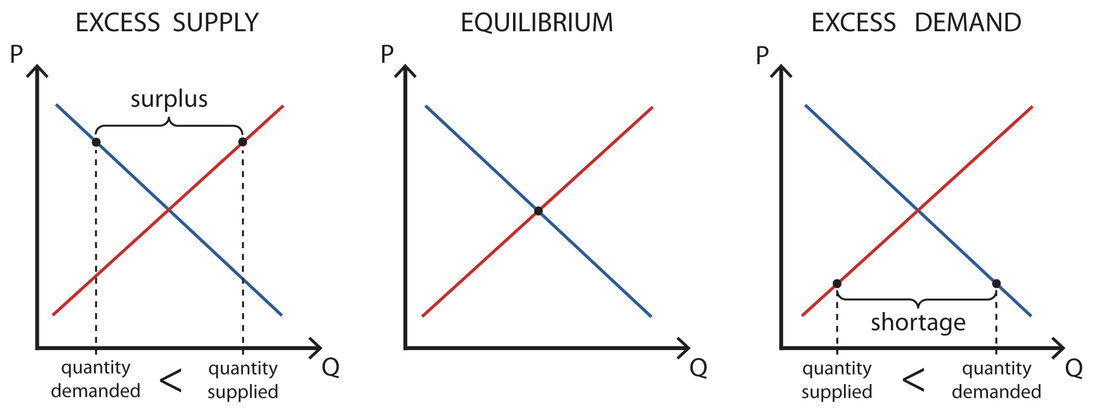

Hi! Today, let's get straight to the point and discuss about the core concepts in economics. 1. Markets 2. Supply and Demand 3. Elasticity MARKETS Let's start with markets. According to investopedia.com, a market is defined as "A medium that allows buyers and sellers of a specific good or service to interact in order to facilitate an exchange.", a market is not always a physical place. An economy consists of many different markets. With no markets, there would be no cash flowing or products switching hands, meaning no economy. SUPPLY AND DEMAND Now, one of the basic concepts that affect a market is the concept of supply and demand. Simply speaking, supply refers to the quantity of services or products available while demand refers to the quantity desired or wanted by the people. Through analysis, these two factors can be used in great effect to identify and find the price of a particular product. Let's divide the concept into two: the law of demand and the law of supply. The law of demand states that when the price of a product rises, the quantity demanded of that product also goes down. In other words, price and quantity demanded are inversely related. Demand can be shown either via a demand schedule (table form) or a demand curve (graph form)  An example of a demand curve. Note the inverse relationship between P ("Price") and Q ("Quantity"). The law of supply on the other hand states that when the price rises, the quantity supplied of that product also goes up. In this sense, price and quantity supplied are directly related. Supply can be shown either via a supply schedule (table form) or a supply curve (graph form).  An example of a supply curve. Note the direct relationship between P ("Price") and Q ("Quantity"). When price is changed, the effect on the demand or supply is represented in the graphs by a movement along the line. Supply and demand however, are subject to shifts too. A shift in supply or demand is different from a movement because it isn't price that is affecting the demand/supply but rather, other factors such as the number of buyers, consumer preference, technology, etc. When we grasp supply and demand completely, we can then graph them together to form the graph for the market of a particular product. With the market graph, we are able to assume the market equilibrium. A market equilibrium is achieved when the quantity supplied and quantity demanded meet, shown in graph form as the intersection of the demand curve and supply curve. It is the ideal goal for most products as the consumers' demand is met yet at the same time, the suppliers do not waste any resources, therefore the market is in its most efficient state. The opposite of an equilibrium is a disequilibrium, wherein the market is inefficient. There are two kinds of market disequilibrium - shortages and surpluses. Shortages are when the supply is not enough to satisfy the demand of a product, on the other hand, surpluses are when your supply exceeds that of the demand, meaning not all your products are sold. Simply speaking, a shortage is when you have too little supply and a surplus is when you have too much supply. A shortage is portrayed in a graph when the point is below the market equilibrium while a surplus is above the market equilibrium as shown below. In summary, demand and supply govern the price of products and market equilibrium is the ideal goal for products wherein demand and supply match perfectly and everyone is satisfied. However, most of the time, the market is in disequilibrium - either shortages or surpluses - and the price should move towards equilibrium.  Market graphs for SURPLUS, EQUILIBRIUM and SHORTAGE. ELASTICITY

The next major concept is elasticity. Elasticity is a very broad term however, we're only tackling the price elasticity of supply and demand. Price elasticity of supply/demand is the responsiveness of the supply/demand when the price is changed. A product is elastic if the demand or supply shifts considerably due to a price change. Inversely, if the product's supply or demand is not affected significantly by the price change, then it is considered inelastic. Like supply and demand, elasticity also has determinants to shifts. An example is whether a product is a necessity or a luxury. Luxury products like iPhones, watches and shoes are usually considered elastic because as they are not essential to life, if prices are raised, significantly less people would buy it. On the other hand, necessities like water and electricity are inelastic because no matter the price change, people would still buy them as they are essential. CASE ANALYSIS - MARKET FOR RICE IN THE PHILIPPINES Now, let's examine a product where we can apply all these concepts. Let's look at the market for rice in the Philippines. Rice is considered a necessity in every household in Asia, most especially in the Philippines. It is present in almost every Filipino meal and is a staple food, therefore we can conclude that the demand for rice is extremely high. Regarding the supply of rice, until very recently, we have had a shortage of rice - becoming increasingly dependent on imports from countries like Vietnam to supply our rice. If there is a shortage, we can assume that the price of rice has increased. According to the Official Gazette of the Philippines, the price of rice was 40.57 pesos per kilo in 2014. However, a recent report by the Philippine Star, dated July 21 2015, has indicated that the price of rice is now 32 pesos per kilo. Both sources suggest that the decrease in the price of rice can be attributed to the present abundance of supply in rice that is actually leaning towards a surplus. However, remember that products can either be elastic or inelastic. In the Philippines’ case, rice has an elastic demand because it is considered a necessity by most Filipinos, therefore we conclude that demand will not be affected by price and people will still buy rice regardless. Hopefully, the analysis of rice has helped you understand the various economic concepts I’ve discussed today but more importantly, help you realize economic problems such as this one and analyze them in a basic manner. Thanks for reading! Sources: Domingo, R. (2015, January 3). PH seen importing 1.8M tons of rice in 2015. Retrieved August 28, 2015, from http://business.inquirer.net/184385/ph-seen-importing-1-8m-tons-of-rice-in-2015 Valencia, C. (2015, July 21). Rice supply abundant, no additional imports eyed. Retrieved August 28, 2015, from http://www.philstar.com/business/2015/07/21/1479080/rice-supply-abundant-no-additional-imports-eyed Rice prices decline by P2 per kilo | Official Gazette of the Republic of the Philippines. (2015, March 25). Retrieved August 28, 2015, from http://www.gov.ph/2015/03/25/rice-prices-decline-by-p2-per-kilo/ Image Sources: http://www.shmoop.com/supply-demand/supply-curve.html http://www.shmoop.com/supply-demand/demand-curve.html http://www.policonomics.com/supply-and-demand/  Economics. I know it sounds so boring and irrelevant to our life but trust me, the reality is that the word economics encompasses so much more. The word "economics" originates from the Greek word "οἰκονομία " (pronounced "oikonomia") meaning "household management". And no, I'm not referring to household chores (ugh). We can define economics as the study of how society (that's us as a whole) manages its' resources or more simply, the study of economies. However, what is fascinating is that economics is truly about the study of people. In this way, economics is wildly complex. But also in this way, we learn to predict one of the most unpredictable species, humans, when faced with situations related to resources. This is what makes the Greek origin of the word so ironic because currently, Greece's government is in economic turmoil. I won't delve into it but for a very simple explanation, it's a result of their massive debt. This also points us to why exactly economics is so important, lack of knowledge and action regarding the study of economics may lead to crises such as Greece's. Therefore, it's kinda imperative to learn about economics - but that's only considering the larger and international scale of economics. Believe it or not, we use economics in our daily lives as well.

Yep. Most of the time, it's unintentional. You see, decision-making is one of the most vital concepts studied in economics. And who doesn't make decisions every day? "Am I going to read past the first paragraph of this blog?" is a decision you just made. Congratulations, you're one step closer to being a teen economist. Anyway, as I said, the human factor is one of the most important - if not the most important - things to consider when discussing economics. To understand the relationship of humans and our decision making skills with regards to economics, we turn to esteemed economist Gregory Mankiw. Gregory Mankiw, Professor of Economics in Harvard University, is one of the most respected and known economists in our time. He's contributed to a lot in economics but for now we'll delve into Mankiw's Ten Economic Principles, more specifically on the four economic principles regarding on how people interact. 1. People face tradeoffs 2. The cost of something is what you give up to get it 3. Rational people think at the margin 4. People respond to incentives "People face tradeoffs" I'd like to place focus and emphasis on this one as it's probably the most important of the four. Simply put, this statement tells us that people are always faced with decisions and that we always give something up when we make a choice. We see the truth in these words in our daily lives, from choosing what to eat for lunch to deciding whether to play with friends or do your homework. In a local context, the Filipino government is faced with tradeoffs all the time and sometimes it affects the people subtly and other times it affects us drastically. The government, and this doesn't only apply to the Philippines but other countries as well, has limited resources and due to this scarcity, are often forced to make decisions that drive us towards objective A but away from objective B. For example, when the government chooses to invest in arms, guns and the country's military, the government is given scarcer or lesser resources to invest in education, health care, agriculture, etc. "The cost of something is what you give up to get it." This reinforces principle number one, that we always give something up when we choose one choice over another but this also tells us that the resources we deal in aren't just limited to physical items like money or food but also include time and effort as well. Every action we do has an "opportunity cost". The economic term "opportunity cost" is whatever we forego whenever we make a choice. Your opportunity cost by reading this blog can be time browsing Facebook and Instagram. Another example, this morning I had a choice to eat ice cream or pancakes, I chose pancakes therefore my opportunity cost is the ice cream and everything else on the menu that I could potentially have eaten. "Rational people think at the margin" As decision-makers, this tells us that we should "think at the margin". To think at the margin is to think one step ahead. Being rational entails that we have to base our decisions on it's cost and benefits such that the benefits of the choice outweighs the opportunity costs. We must also analyze our choices and think ahead of them. What are the consequences of this choice? Will this choice lead to other choices? To think like an economist, we must consider these various questions. "People respond to incentives" Ever come across a sale in a popular clothing store then suddenly blowing all your money and going on a shopping spree because "it was 50 percent off"? That's you responding to an incentive. An incentive can be a bonus, special offer, a discount on products or could be moral and natural indentives wherein a person is driven by their morals, self-esteem, curiousity and their emotions. As human beings, we all try to take advantage of these incentives. It's these incentives that drive you forward and can be used as a tool to increase your performance. Want a pay raise or promotion? You have to work harder. The decision to work harder is fueled by that pay raise. A social issue we can use as an example to analyze would be the ASEAN integration for the Philippines. The ASEAN (Association of South East Asian Nations) aims to integrate the region and create an ASEAN Economic Community (think European Union). At first, it sounds perfect, more jobs, lower tax, easier transport between ASEAN countries, etc. but we learned that everything has a tradeoff and this is no exception. The integration, if we choose to accept it, will essentially open borders to other countries in an economic sense, and if we think at the margin, we introduce other, bigger, foreign companies in our local area. These better companies will overshadow our own local companies and lessen the opportunities for small Filipino businesses in this country. Also, when we remember that people respond to incentives and remember that other countries have better opportunities and jobs in store for our local workers, we realize that we will lose our smartest and most deserving citizens to other countries who offer better jobs than the Philippines, this is actually a pretty big issue now with the massive amount of OFWs (Overseas Filipino Worker) we have right now. My personal opinion however, is that we should accept the ASEAN integration because we are prepared for it and the marginal benefits outweigh the marginal costs. In conclusion, economics is important and relevant in our daily life because it allows us to see how people interact with decisions. We always face tradeoffs because there is always an opportunity cost to our choices, whether it be physical materials or the time to commit to it. To be rational decision-makers, we should realize that we need to think ahead of our choices and what roads it leads to and remember the fundamental fact that people will always be moved and motivated by incentives. Sources: Retrieved from: http://www.mb.com.ph/implications-of-the-asean-economic-community-first-of-two-parts/ Masigan, A. (2014, October 5). Implications of the ASEAN Economic Community. Retrieved July 19, 2015. Retrieved from: http://www.forbes.com/sites/investopedia/2012/08/21/the-role-of-opportunity-cost-in-financial-decision-making/ The Role Of Opportunity Cost In Financial Decision Making. (2012, August 21). Retrieved July 19, 2015. Mankiw's Ten Principles. (n.d.). Retrieved July 19, 2015, from http://www.swlearning.com/economics/mankiw/principles2e/principles.html Margins and Thinking at the Margin. (n.d.). Retrieved July 19, 2015, from http://www.econlib.org/library/Topics/College/margins.html Image retrieved from: http://i.kinja-img.com/gawker-media/image/upload/czcmmcsfz7pqehjuzmst.jpg |

AuthorHi, I'm Gabriel, a high school student at Xavier School writing this blog about economics aimed towards teenagers. Have fun! Archives

October 2015

Categories |

RSS Feed

RSS Feed